The U.S. government may be tempted to restrain gold prices, but this would only serve to drive bullion higher, according to the latest GREED & fear report from Christopher Wood, Global Head of Equity Strategy at Jeffries.

Wood wrote that there is an “obvious temptation on the part of a major central bank to seek to try to manage the gold price,” and shared an anomalous move in Comex gold futures as an example of how this kind of management might appear.

“At 3pm New York time last Thursday there was a US$1.6bn sale of gold futures in about three minutes which temporarily knocked the bullion spot price,” he pointed out, and while he has no idea who was behind it, he noted that “a soaring gold price is not in the interest of the relevant authorities any more than a surging oil price is.”

Wood wrote that while the drivers of the oil price rally are fairly obvious, “the near-term drivers of the current gold rally are much less clear.”

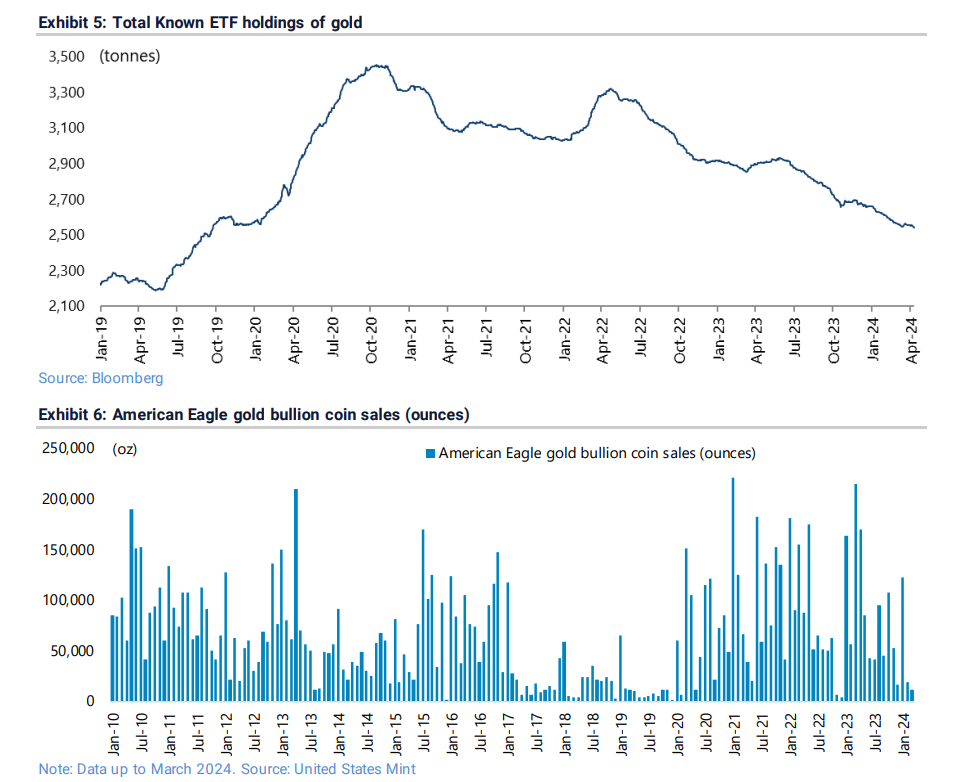

“For now at least there continues to be a notable lack of inflows into gold ETFs in the Western world,” he noted. “Rather the reverse is the case. There is also no evidence of a sudden pickup in sales of American Eagle Bullion coins, one of the most popular series in the US.”

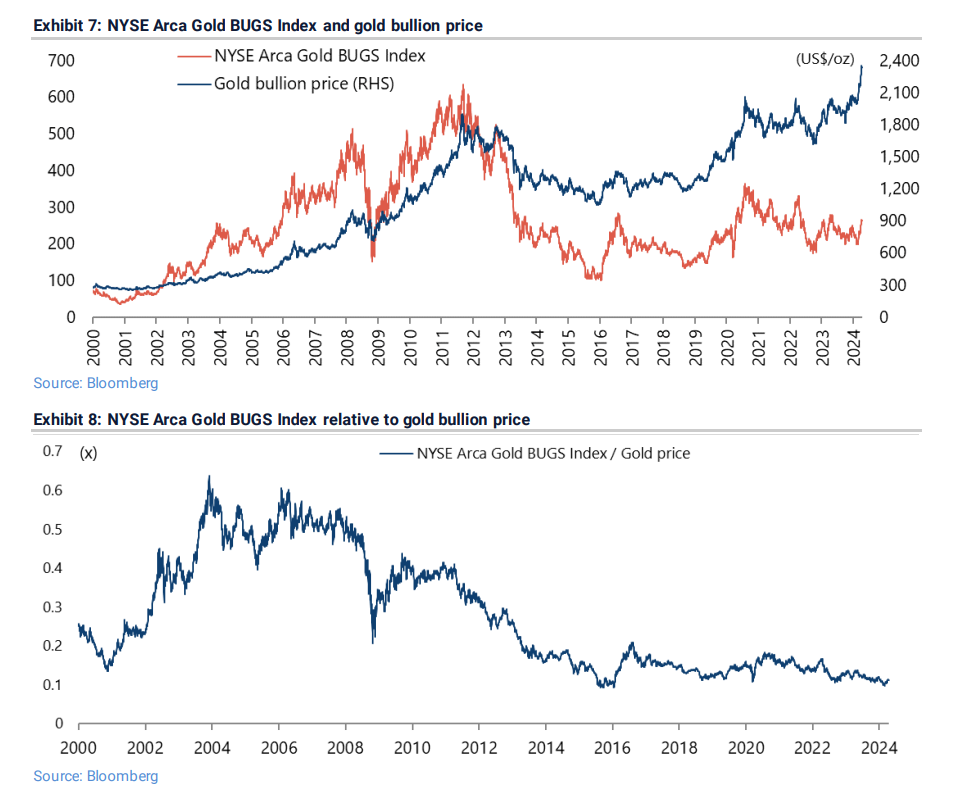

Wood also noted that despite their recent gains, gold mining stocks “are not really outperforming bullion on the scale which would normally be expected to happen in a roaring bull market” like they did in 2001 – 2011. “Gold mining stocks also remain extremely cheap based on the current bullion price,” he said.

“If all of the above shows a distinct lack of investor euphoria as regards gold, the question remains what is driving the current rally,” he said. “The most plausible explanation remains demand from China. Still there is a lack of concrete data to confirm such an explanation. True, the PBOC has bought gold for 17 months in a row according to the official foreign reserves data. But there is a lack of hard data on retail demand for gold.”

Wood said it’s impressive that gold continues to set new record highs without ETF inflows in the West. “While this latter point clearly highlights that there is a risk to the current rally, probably the biggest risk remains official attempts to manage the price down,” he said.

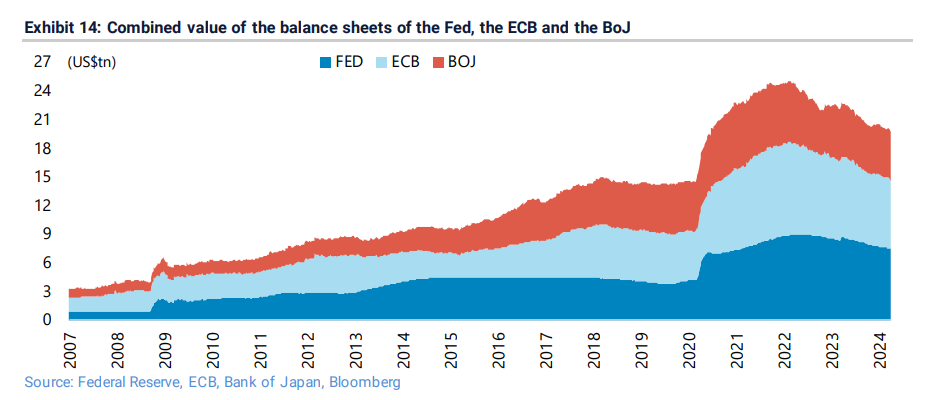

He said the real issue “is less why gold is rising now than why it has not risen by much more in recent years when G7 central banks in the quanto easing era have engaged in increasingly aggressive monetisation as reflected in the extraordinary expansion of their balance sheets.”

Wood also noted that the short duration of the debt held by the U.S. federal government is “in stark contrast to the duration of the government debt of other G7 governments,” nor does it align with the situation in U.S. investment-grade corporate bonds.

“The best explanation for this growing reliance on short-term funding on the part of the federal government is that it reflects the natural complacency encouraged by the privilege of printing seemingly at will the world’s reserve currency,” he said. “But that privilege, in the context of the political reality of the rise of the formal BRICS grouping and the commercial reality of growing evidence of trade conducted outside the dollar, is not cast in stone.”

“These growing pressures, and the policy responses they may trigger, are as good a reason to own some gold as any,” Wood said. “In the case of the fiscal situation, the ultimate temptation in Washington could well be to try and fix longer dated bond yields in some US version of yield curve control which would surely be as gold bullish as it would be dollar bearish. This is why official efforts to manage the price of gold in the above context risk backfiring.”

Source: Ernest Hoffman Kitco