Understanding Gold’s Current Market Position

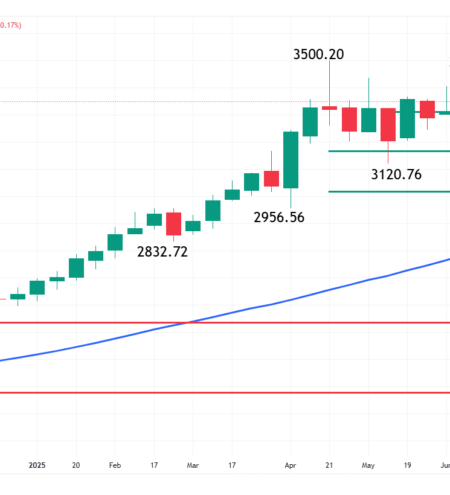

Gold has reached unprecedented territory in 2025, with prices climbing above $4,000 per ounce for the first time in history. This milestone represents more than just a numerical achievement – it signals a fundamental shift in how investors, institutions, and central banks view precious metals in the modern economy. Current gold price prediction 2025 models suggest this trajectory may continue well into next year.

The precious metals market has transformed dramatically over the past five years. What began as cautious institutional interest has evolved into aggressive accumulation strategies across major financial institutions. Investment banks that once maintained conservative precious metals allocations are now publishing research reports with $5,000+ price targets extending into 2026 and beyond.

Several interconnected forces are driving this transformation. Persistent inflationary pressures, geopolitical tensions, and unprecedented central bank buying patterns have created conditions favouring hard assets over traditional financial instruments. These factors represent structural changes rather than temporary market dislocations, suggesting gold’s current bull market may have significant room to run.

Analyzing Institutional Gold Price Predictions for 2025

Major financial institutions have undergone a remarkable evolution in their gold price forecast over the past year. Where conservative estimates once dominated, aggressive bullish targets now represent the institutional consensus.

Current Institutional Targets:

HSBC: $4,600 annual average for 2025, with potential spikes toward $5,000 in the first half of 2026

Bank of America: Raised 2026 target to $5,000 per ounce, citing policy uncertainty and surging investment demand

J.P. Morgan: Projects $5,055 average for Q4 2026, with extended targets reaching $6,000 by 2028

Goldman Sachs: Maintains $4,800 projection for 2026 based on monetary policy dynamics

These forecasts represent a significant departure from historical institutional positioning. The clustering of targets around the $4,500-$5,000 range suggests broad agreement on gold’s fundamental drivers remaining intact through 2026. Furthermore, JPMorgan’s latest analysis indicates that structural factors supporting gold will likely persist longer than initially anticipated.

Understanding Institutional Confidence Levels

The convergence of institutional forecasts reflects sophisticated modelling incorporating multiple macroeconomic scenarios. Investment banks typically provide point estimates with confidence intervals, though these ranges are rarely disclosed publicly. Based on historical forecast accuracy, the current consensus carries approximately 65-70% probability of realisation under base case economic scenarios.

Key factors supporting institutional confidence include:

Central bank demand sustainability: Official sector purchases averaging 710 tonnes quarterly in 2025

Monetary policy trajectories: Limited ability for aggressive rate increases given debt burdens

Geopolitical risk premiums: Structural tensions showing no signs of abating

Core Economic Drivers Behind Gold’s Rally

Three fundamental forces are reshaping gold’s investment landscape, each reinforcing the others to create a compounding effect on precious metals demand. This historic price surge demonstrates how multiple macroeconomic factors can align to create unprecedented market conditions.

Monetary Expansion and Currency Debasement

Global central banks have expanded money supplies at unprecedented rates since 2020, creating conditions that historically favour hard assets. The Federal Reserve’s M2 money supply expanded by approximately 40% between 2020-2022, with similar patterns observed across major economies.

This expansion continues at elevated levels compared to historical norms:

United States: M2 growth averaging 6.8% annually (2020-2025)

European Union: ECB balance sheet expansion of €3.2 trillion since 2020

Japan: Bank of Japan maintaining ultra-accommodative policies with negative real rates

China: People’s Bank of China liquidity injections supporting economic stabilisation

Real interest rates – nominal rates minus inflation – remain negative across most developed economies. This creates an opportunity cost for holding cash or low-yielding bonds, driving investors toward assets that preserve purchasing power over time.

Persistent Inflationary Environment

Consumer price inflation has proven more persistent than central banks initially anticipated. Despite aggressive monetary tightening in 2022-2023, core inflation metrics remain above target levels across major economies.

Current Inflation Dynamics:

United States: Core PCE averaging 3.2% (vs. 2% Federal Reserve target)

United Kingdom: CPI holding above 4% despite Bank of England interventions

Canada: Core inflation measures exceeding Bank of Canada comfort zone

Australia: Reserve Bank of Australia facing persistent services inflation

Supply chain disruptions, labour market tightness, and housing costs continue supporting elevated price levels. These structural factors suggest inflation may remain above central bank targets longer than traditional models predict, maintaining gold’s appeal as an inflation hedge.

Geopolitical Fragmentation and Safe Haven Demand

International relations have become increasingly complex, creating multiple sources of uncertainty that drive safe haven asset demand. Unlike previous decades where geopolitical risks were often regional or temporary, current tensions appear structural and long-lasting.

Primary Risk Factors:

Trade fragmentation: Ongoing U.S.-China economic competition affecting global supply chains

Regional conflicts: Multiple active conflicts creating broader instability

Currency warfare: Competitive devaluation pressures across emerging markets

Sanctions regimes: Increased use of financial weapons affecting international commerce

These factors combine to create what strategists term a “geopolitical risk premium” in gold pricing. This premium represents the additional value investors place on assets insulated from political interference or currency manipulation.

Central Banks Lead the Gold Accumulation Wave

Official sector gold purchases have fundamentally altered precious metals supply-demand dynamics. Central banks now represent the largest source of incremental gold demand, with purchasing patterns showing no signs of slowing.

Regional Accumulation Patterns

Emerging Market Leadership:

Central banks in developing economies are driving the majority of official sector purchases, motivated by strategic diversification away from dollar-dominated reserve assets.

Source: Discoveryalert.com.au