Gold’s price decline since Trump’s electoral victory is as much about the party as it is the candidate, while global silver demand from the solar industry continues to rise as technology evolves and countries surpass their installation targets, according to precious metals analysts at Heraeus.

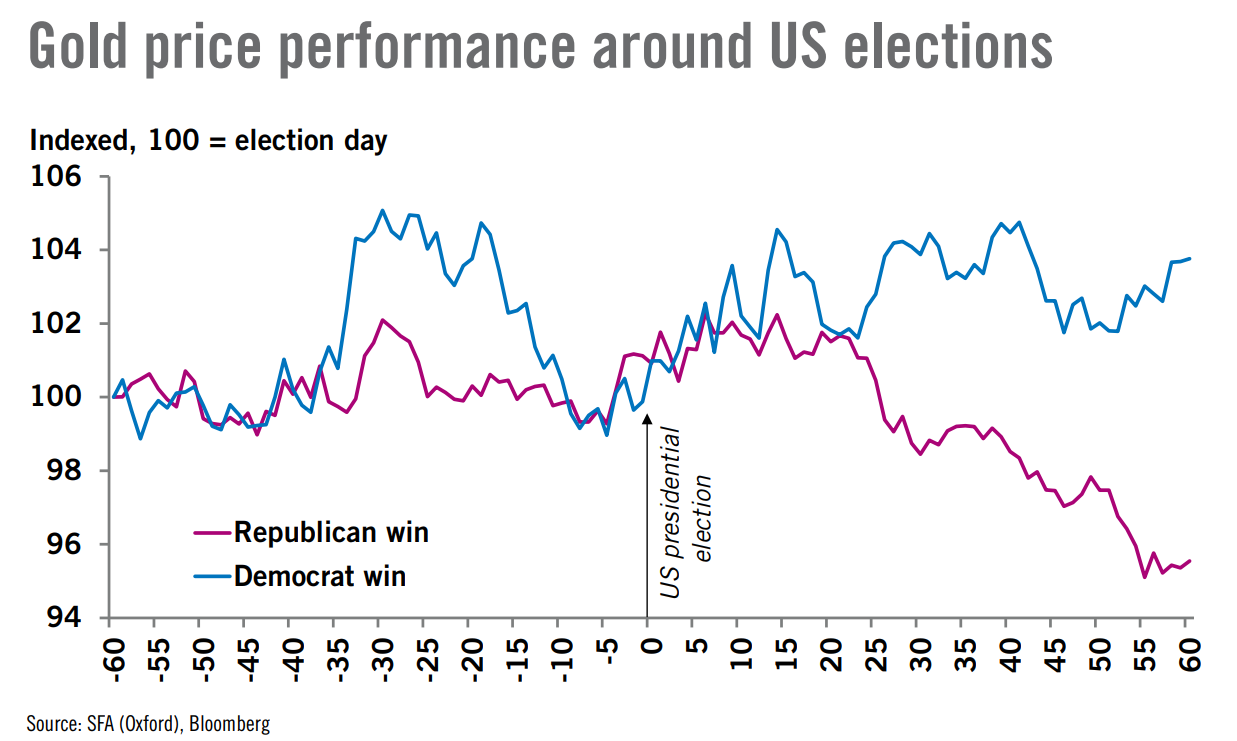

In their latest precious metals update, the analysts noted that historically, Republican victories have not been good for gold’s near-term prospects.

“Gold dropped to $2,643/oz, the lowest price in 19 days, and the dollar strengthened as it became clear that Trump would return as US president,” they wrote. “The dollar index saw more than a 1% gain against most major peers on the day of Trump’s win. Following the 2016 Trump victory there was an 11.6% fall in the price of the yellow metal.”

The analysts pointed out that the slide in precious metals prices was not all about Trump. “Since 1976, election of a Republican administration has led to an average 4.5% decline in the price of gold within 60 days compared to an average 3.8% rise for a Democrat win,” they said. “Likely control of the House of Representatives and confirmed Republican control of the Senate increase the likelihood of conservative economic policy implementation and reduce uncertainty in geopolitical direction, but not the details.”

“As a safe-haven asset, gold tends to rise in a highly uncertain environment,” they wrote. “However, probable execution of import tariffs and tax-cutting policies could stoke inflation and expand the federal deficit. The Federal Reserve’s rate cutting path – which was restated on Thursday by the expected 25 basis points – may have to slow or change if inflation rises. This outcome would support safe-haven demand on a slightly longer-term outlook.”

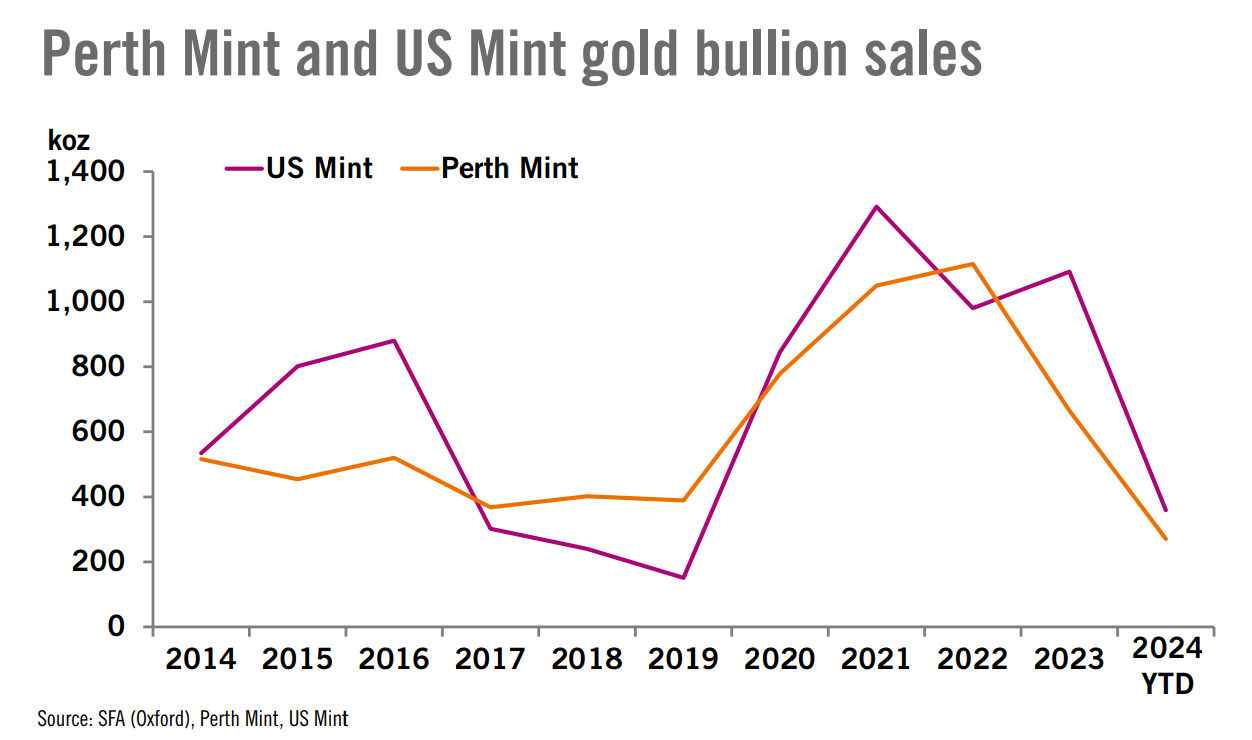

Heraeus also noted large year-over-year declines in bullion sales at both the U.S. and Perth Mints. “Cumulative totals up to October show a 663.5 koz decline in purchases of gold bullion from the US Mint in 2024 compared to 2023,” the analysts said. “This puts US Mint sales on track for the weakest year since 2019 when only 151 koz was bought. Similarly, purchases from the Perth Mint were down 261 koz by September 2024 compared to the same time last year. Notably, 2023 sales from the Perth Mint were 40% down from 2022 to 665 koz.”

“This all represents a year-on-year continuation in decline in retail buying for both mints which fits with the larger trend globally,” they added. “Bar and coin investment was down 9% year-on-year as of Q3’24. Notably, the decline in this metric accounted for by the US and Perth Mints was offset by India, Korea and Taiwan where buying was up 41%, 36% and 28% year-on-year, respectively (source: World Gold Council). Even with strong gains in these countries, retail investment demand is down and may continue to struggle if the gold price stays high.”

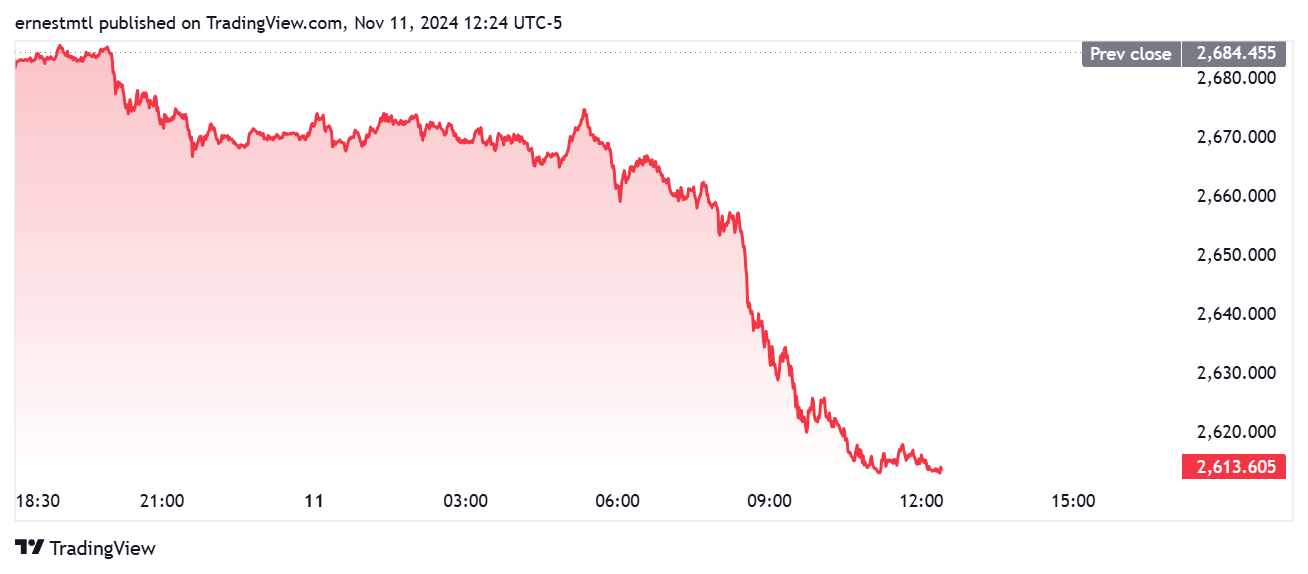

Gold prices have set a session low of $ 2,612.74 and are hovering just barely above that level at the time of writing. Spot gold last traded at $2,613.61 per ounce for a loss of 2.64% on the session.

Turning to silver, Heraeus said that solar continues to absorb supply, with expanding solar capacity and a shift in technology increasing the industry’s demand for the gray metal.

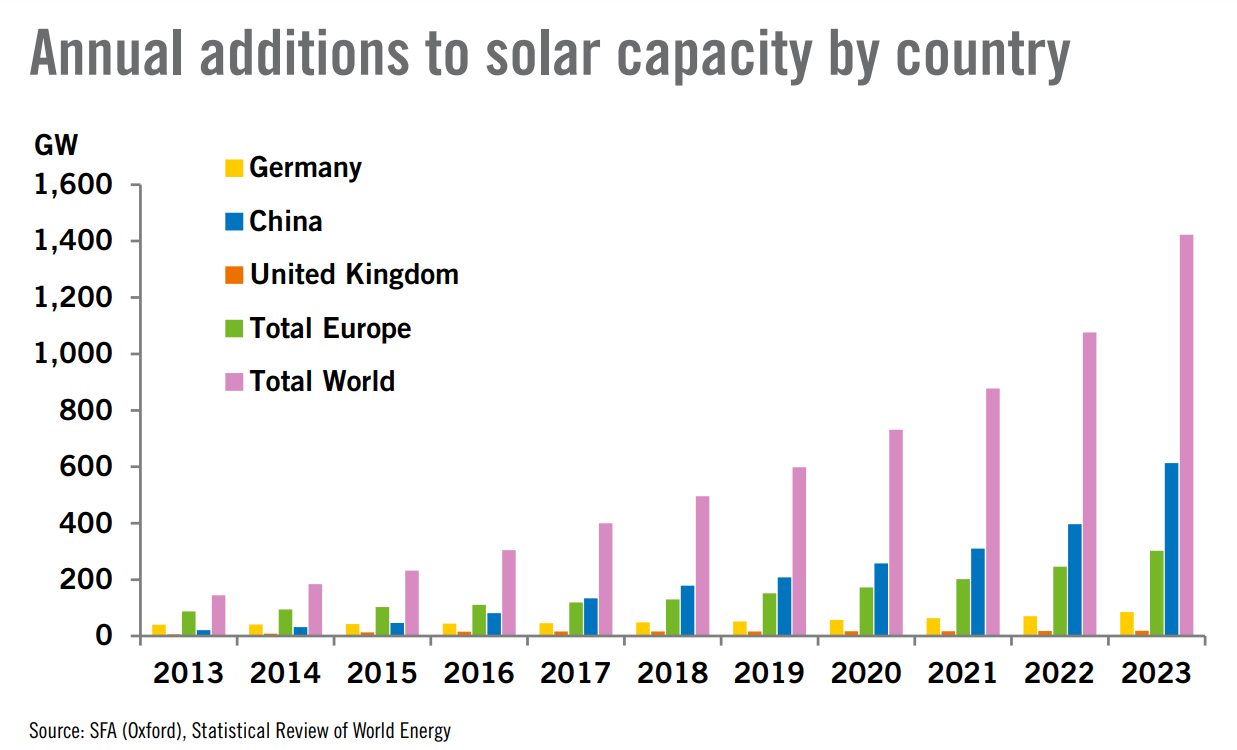

“Last week, the UK’s National Energy System Operator (NESO) called upon the UK government to have 47 GW of solar capacity in the UK by 2030,” the analysts said. “UK solar capacity reached 17 GW as July 2024 drew to a close (source: Department for Energy Security and Net Zero). Recorded capacity in July 2024 was 1.2 GW higher than in July 2023, so to meet the aspirations of NESO the UK must increase its annual rate of solar deployment by nearly four-fold.”

They noted that the growth rate in Germany is even higher than in the UK, while Chinese solar growth blows both out of the water. “In Germany, 10.23 GW of photovoltaic capacity was added in the first eight months of 2024, bringing the cumulative total to 93.02 GW,” the analysts wrote. “The EU is expected to install 401 GW of new solar between 2024 and 2028, potentially bringing the total to 671 GW. Meanwhile, the Chinese solar industry added 102.48 GW of capacity in the first half of 2024 alone, making the current total 711 GW and representing an unmatched 140% year-on-year growth. China is on track to exceed its 2024 expectation, laid out by the Energy Institute, of installing 165 GW of capacity.”

Asia is also driving the shift from P-type to N-type cells, which require more silver in their production. “Despite improved thrifting and substitution with cheaper metals, such rapid installation growth and the rising use of N-type cells should continue to bolster silver demand in 2024,” they said.

The growth of the solar industry around the world is a string positive for silver demand going forward, they added. “Global capacity additions this year are forecast to be 550-600 GW compared to 2023 when 447 GW was installed,” the analysts wrote. “Worldwide total demand for silver was 1,195 moz in 2023, of which photovoltaics consumed 14%. Total demand is expected to rise modestly to 1,200 moz in 2024. However, this increase in demand from the solar sector could push overall demand higher in 2024.”

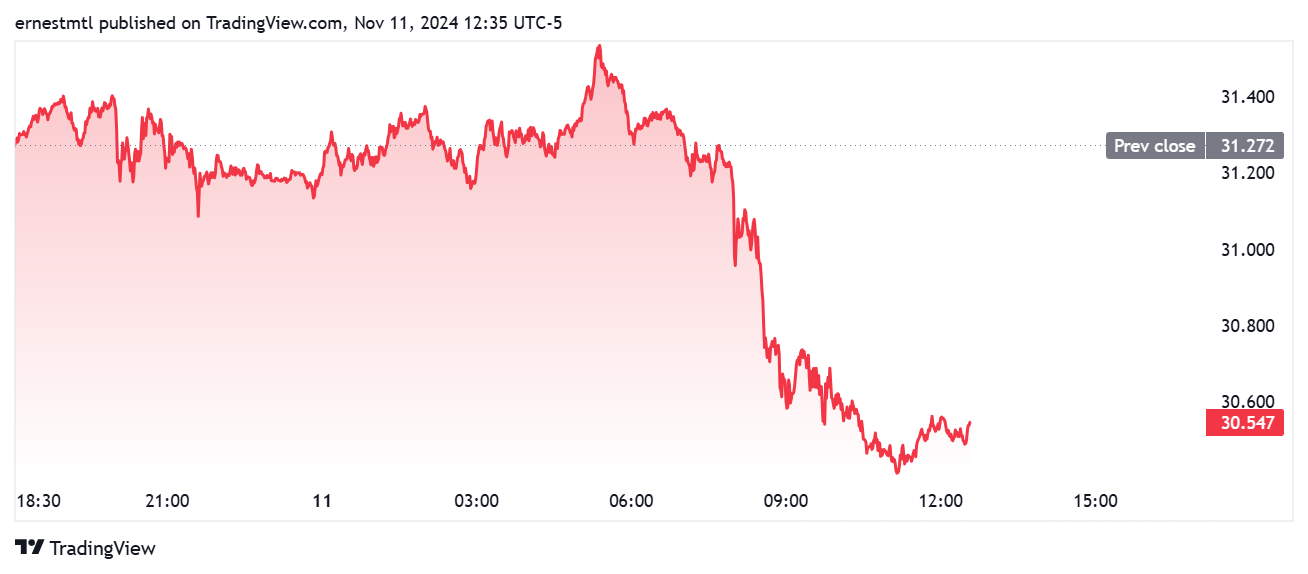

But despite these medium and long-term demand projections, silver prices have followed gold lower since Tuesday. “Like the rest of the precious metals, the silver price dropped last week, falling back below $32/oz,” they wrote. “By Friday’s close it had retraced comfortably below this key level to $31.27/oz.”

Silver prices have continued their recent downward trajectory on Monday, At the time of writing, spot silver last traded at $30.547 per ounce and is down 2.32% on the daily chart.